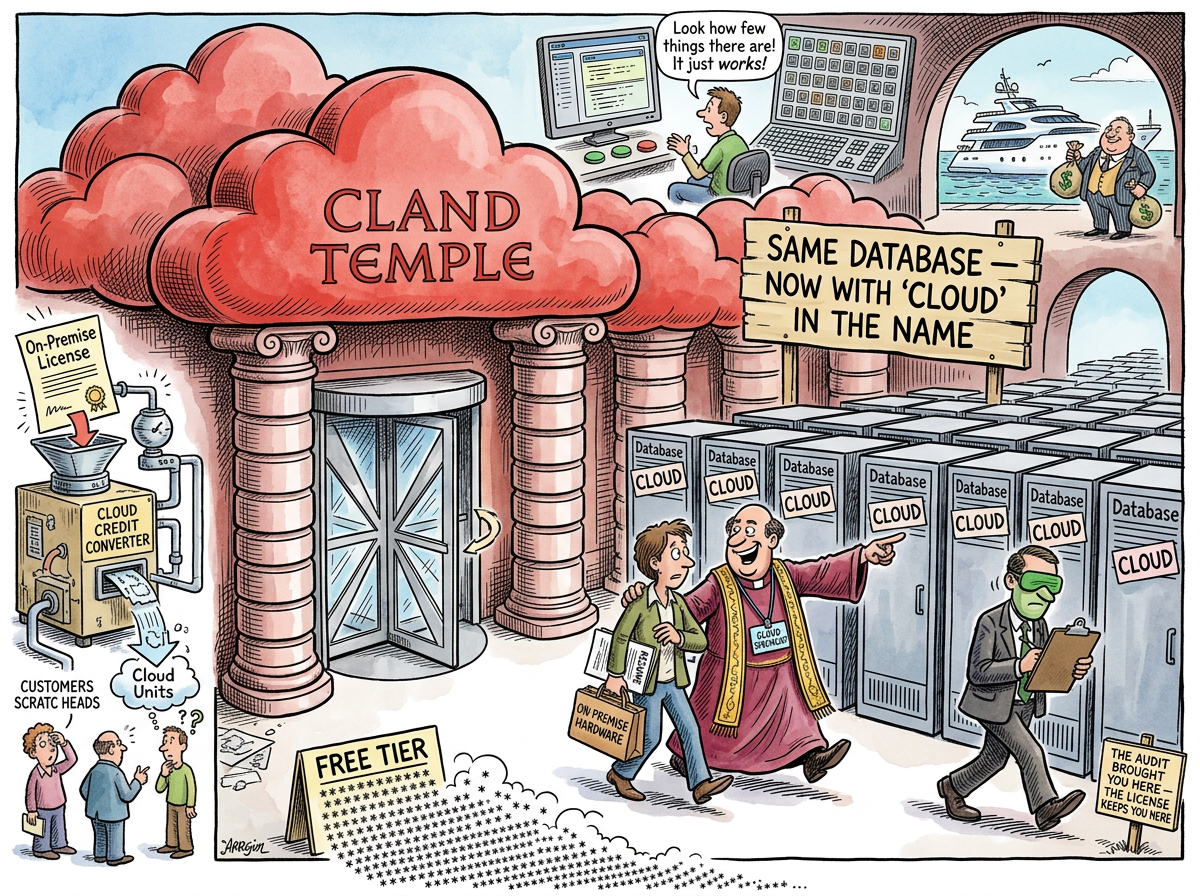

Oracle Cloud (OCI, Oracle Cloud Infrastructure) is Oracle’s cloud computing platform, which should not be confused with Oracle the database company, although the confusion is understandable because Oracle Cloud exists primarily to ensure that Oracle database customers remain Oracle database customers, now with the word “cloud” on the invoice.

Oracle Cloud launched in 2016, approximately a decade after AWS, and entered a market where AWS, Azure, and GCP had already divided the territory. The strategic response was not to compete on breadth of services (impossible), developer experience (improbable), or brand affinity (Oracle has negative brand affinity among developers). The strategic response was to compete on the one axis where Oracle has an unassailable advantage: existing Oracle database licenses.

If you already run Oracle Database, migrating to Oracle Cloud is cheaper than migrating to AWS, because Oracle’s licensing terms penalise customers who run Oracle on non-Oracle clouds. The per-core licensing factor on AWS is 2x. On Oracle Cloud, it is 1x. This is not a discount. This is a surcharge on leaving.

The Licensing Gravity Well

Oracle Cloud’s customer acquisition strategy is best understood as a gravitational assist, using the mass of existing Oracle licensing to redirect customer trajectories toward OCI:

- Customer runs Oracle Database on-premises

- Customer’s on-premises hardware reaches end of life

- Customer considers AWS (natural choice, largest cloud)

- Oracle’s licensing terms double the per-core cost on AWS

- Oracle sales offers “Bring Your Own License” to OCI at 1x

- Customer discovers that migrating to OCI is “free” (minus the three-year commitment)

- Customer migrates to OCI

- Customer is now an Oracle Cloud customer

- Customer was always an Oracle customer

Step 9 is the key: Oracle Cloud does not acquire new customers. Oracle Cloud retains existing customers by making the alternative more expensive. This is lock-in as a service — the logical evolution of Oracle’s forty-year business model, now available in cloud form.

The Actually Good Parts

The uncomfortable truth about Oracle Cloud is that the infrastructure is genuinely competitive.

OCI’s compute is priced aggressively — often 30–50% cheaper than equivalent AWS instances. The networking is simpler (no data transfer charges between availability domains within a region, unlike AWS’s nickel-and-diming). The bare-metal instances are real bare metal, not virtualised servers pretending to be bare metal. The Autonomous Database genuinely manages itself.

Oracle hired good engineers. Oracle built good infrastructure. Oracle then marketed it with the Oracle brand, which is the technological equivalent of baking an excellent cake and delivering it in a hearse.

Developers who have actually used OCI — a population small enough to fit in a conference room — consistently report surprise at its quality. The console is cleaner than AWS’s. The pricing is more transparent than Azure’s. The free tier is generous (a permanent free Arm-based VM with 24GB RAM is the best free tier in cloud computing).

None of this matters, because the brand is Oracle, and the developer community’s relationship with Oracle is the technological equivalent of a restraining order.

The Free Tier Paradox

Oracle Cloud’s free tier is the most generous in the industry: always-free Arm compute instances, 200GB of block storage, 10GB of object storage, and an Autonomous Database. The permanent free VM — 4 Arm cores, 24GB RAM — is more powerful than many startups’ paid infrastructure.

This creates the Oracle Cloud paradox: the best free tier in cloud computing, offered by the company developers trust least. The free tier exists to create adoption. Adoption requires trust. Trust requires not being Oracle. Oracle cannot stop being Oracle. The free tier persists, excellent and underused.

The Ellison Factor

Larry Ellison, Oracle’s co-founder and CTO, announced Oracle Cloud’s strategy with the subtlety that characterises all Oracle communications: AWS is yesterday. Oracle Cloud is tomorrow. Every customer will migrate. Resistance is futile.

This was said in 2017. In 2026, AWS’s market share is approximately 31%. Oracle Cloud’s market share is approximately 2%. The prophecy remains unfulfilled, but Oracle’s sales team remains committed to its inevitability, which is the Oracle way: reality is a negotiating position.

Measured Characteristics

- Global market share: ~2%

- Cloud launch year: 2016 (a decade after AWS)

- Licensing factor on OCI: 1x

- Licensing factor on AWS: 2x (effectively a 100% surcharge for leaving)

- Customer acquisition via technical merit: rare

- Customer acquisition via licensing gravity: primary

- Console quality relative to brand reputation: surprisingly good

- Free tier generosity: best in industry

- Free tier adoption: limited by brand trust

- Engineers who have used OCI and were surprised: most of them

- Engineers who will publicly recommend OCI: significantly fewer

- Larry Ellison yacht size relative to OCI revenue: disproportionate