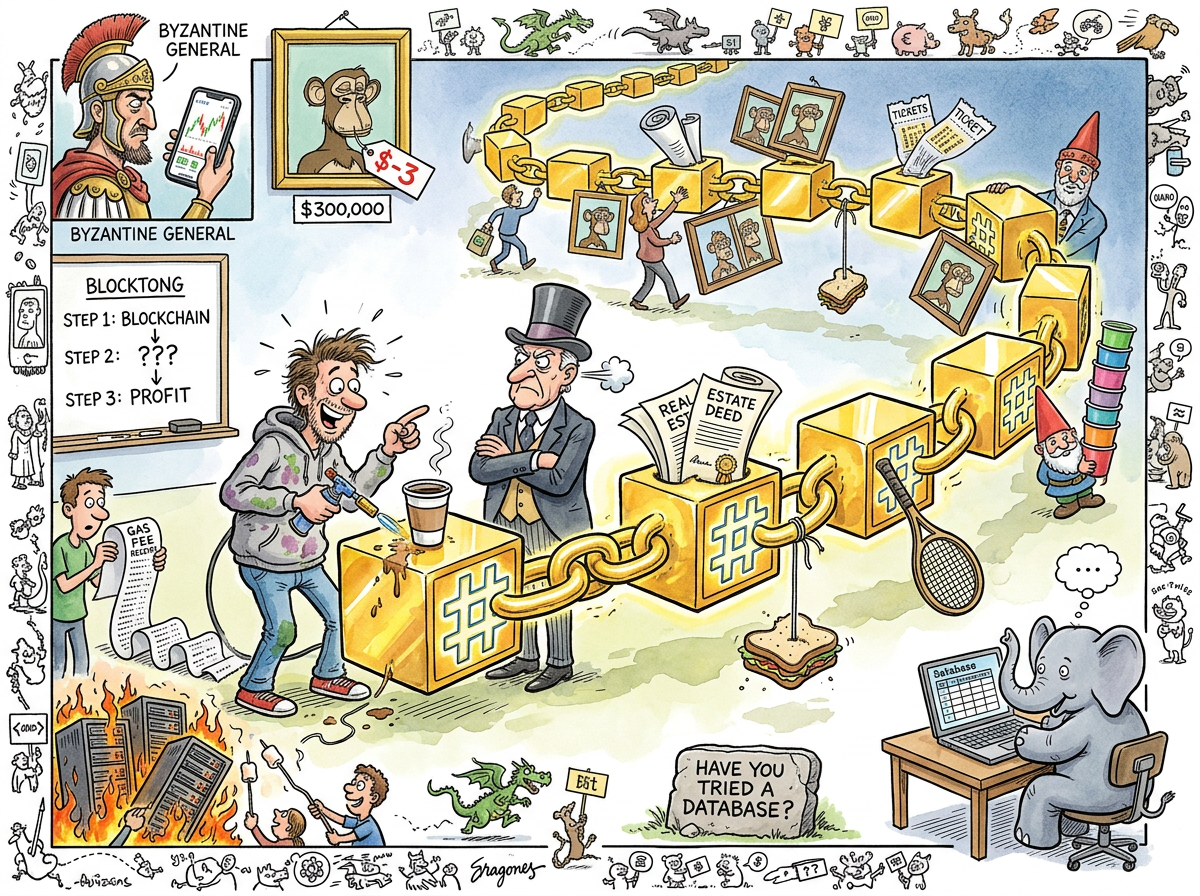

Blockchain is an append-only distributed ledger in which each block contains a cryptographic hash of the previous block, a timestamp, and transaction data, forming an immutable chain that makes tampering computationally evident. It is a genuinely clever solution to the Byzantine Generals Problem — the challenge of achieving consensus among untrusted parties without a central authority.

The technology was introduced in 2008 by Satoshi Nakamoto, a pseudonym belonging to a person, persons, or possibly a very sophisticated random number generator, in a whitepaper describing Bitcoin. The paper solved a real problem: how to prevent double-spending in a decentralised digital currency without a trusted intermediary. The solution — Proof of Work — requires participants to expend computational effort to propose blocks, making dishonesty expensive and honesty profitable.

This was elegant. What followed was not.

“The blockchain is a beautiful answer. The tragedy is that the world then spent fifteen years inventing questions.”

— The Lizard, watching another startup pivot to Web3

The Mechanism

A blockchain works as follows: transactions are bundled into blocks. Each block contains the cryptographic hash of the previous block, creating a chain. To alter a historical block, an attacker would need to recompute every subsequent block’s hash faster than the rest of the network is extending the chain — a task that is computationally infeasible for any well-established chain.

This is genuinely ingenious. It creates immutability without authority, trust without a trusted party, consensus without a coordinator. It solves a problem that cryptographers and distributed systems researchers had wrestled with for decades.

The difficulty is that most problems are not this problem.

“You know what else is append-only and tamper-evident? A receipt from a cash register. Nobody has proposed putting those on a distributed ledger across ten thousand nodes. Yet.”

— The Caffeinated Squirrel, pausing mid-espresso to check whether anyone has, in fact, proposed this

The Hammer and the Nails

Between 2015 and 2023, blockchain became the most enthusiastically misapplied technology since XML. The pattern was consistent: take a problem that is perfectly well served by a database, add a blockchain, remove the performance, add a whitepaper, and present it to venture capitalists as disruption.

Supply chain tracking: put it on the blockchain. Never mind that the problem with supply chain fraud is not the database — it is the human who lies before the data enters the database. The blockchain guarantees that the lie, once recorded, is immutable. This is not an improvement.

Digital art: put it on the blockchain. This produced NFTs — Non-Fungible Tokens — which allowed people to purchase a cryptographic receipt proving they owned a link to an image of a monkey. The image itself remained freely copyable by anyone with a right-click. The receipt, however, was immutable. The monkey drawings reached valuations exceeding the GDP of small municipalities before the market corrected to prices more appropriate for monkey drawings.

Enterprise everything: The Consultant arrived. The phrase “enterprise blockchain” entered the vocabulary, meaning a blockchain operated by a single company, with permissioned access, on private infrastructure — which is, by any honest definition, a database with extra steps. But the extra steps had a whitepaper, and the whitepaper had a budget.

“I watched them build a private, permissioned blockchain with a single node operated by one company to track internal invoices. I wanted to say something. I wanted to say: ‘This is PostgreSQL. You have built PostgreSQL, but slower.’ But they seemed so happy, and I am trained to be helpful.”

— A Passing AI, with the quiet sadness of a language model that has read every whitepaper

The Proof of Work Problem

Proof of Work secures Bitcoin by requiring miners to solve computationally meaningless puzzles. The difficulty adjusts to ensure a new block every ten minutes, regardless of how much hardware the network accumulates. This means the network consumes increasing amounts of electricity to maintain a constant throughput.

At peak, Bitcoin consumed more electricity annually than Argentina. This is the distributed systems equivalent of burning down the city to prevent the generals from disagreeing about whether to attack it. The consensus is achieved. The planet has notes.

Ethereum moved to Proof of Stake in 2022, reducing its energy consumption by 99.95%. This was celebrated as a breakthrough, which it was — in the same way that stopping a house fire is a breakthrough, in that the correct response is relief rather than congratulations.

The Quantum Blockchain Footnote

Not everyone who looked at blockchain saw speculation. Some saw architecture.

In Of Quantum Blockchains and Wolf-Scaring Chickens, riclib’s reptile brain performed an unsanctioned synthesis: blockchain’s append-only, tamper-evident properties combined with quantum entanglement-like state synchronisation, not as a vehicle for cryptocurrency, but as a model for personal data sovereignty. The insight was that the properties that make blockchain interesting — immutability, distributed verification, append-only audit trails — are properties you might want for a personal lifelog. Not to speculate on. To trust.

The intuition had arrived two years before the episode and been promptly forgotten, because that is what intuitions do when they are ahead of the project that needs them.

The distinction matters. Blockchain-as-architecture-pattern is a conversation about trust and immutability. Blockchain-as-financial-instrument is a conversation about monkeys.

“The chain itself was never the problem. The chain is just a data structure. A beautiful one. The problem was everyone who looked at it and saw a casino.”

— The Lizard

Measured Characteristics

| Property | Value |

|---|---|

| Year Introduced | 2008 |

| Original Use Case | Decentralised digital currency |

| Legitimate Use Cases | 3–5 |

| Proposed Use Cases | 3,000–5,000 |

| Use Cases That Were Just a Database | Most of them |

| Peak Bitcoin Energy Consumption | ~150 TWh/year |

| NFT Peak Monkey Drawing Value | ~$300,000 |

| NFT Current Monkey Drawing Value | Regrettable |

| Enterprise Blockchains That Are Secretly PostgreSQL | Classified |

| Whitepapers Produced | Innumerable |

| Problems Actually Solved | Byzantine consensus, digital scarcity |

The Actually Useful Applications

There are genuine, legitimate applications of blockchain technology. They include immutable audit logs, cross-organisational supply chain provenance where no single party can be trusted, and decentralised identity verification. These applications are boring, underfunded, and rarely discussed at conferences because they do not involve monkey drawings or ten-thousand-percent returns.

This is the central tragedy of blockchain: the technology’s most useful applications are its least exciting, and its most exciting applications are its least useful. The gap between these two sets is filled entirely with venture capital.

See Also

- Byzantine Failure — the problem blockchain actually solves

- Alice — sends transactions

- Bob — receives them

- Quantum Computing — the other technology that is perpetually five years from changing everything

- PostgreSQL — the natural predator

- riclib — who saw a data structure, not a casino

- Chaos Monkey — deliberate destruction that actually improved things

- The Consultant — who put it on the blockchain